The Massive Housing Market Risks Nobody Talks About

Perhaps the most common economic commentary circulating today is the fear that the average American family has been priced out of the housing market for the rest of their lives.

Perhaps the most common economic commentary circulating today is the fear that the average American family has been priced out of the housing market for the rest of their lives. Gen Z and even Gen Alpha teens are already planning for a future in which buying a home is impossible. This is not only happening in the U.S.; all across the western world from Australia to Canada to Europe, people are facing the worst home price inflation in decades.

However, just as in physics, there are rules of motion that still apply to markets regardless of government or central bank intervention. What goes up must inevitably come down.

There’s been an interesting development in the past year, specifically on the seller’s side of the housing equation. During the pandemic, the relocation panic, Covid stimulus and corporate buyers drove up prices across the board and the average cost of a home skyrocketed by 50% from 2019 to 2024.

A large portion of this buying was internal migration (mostly away from blue states). At the same time, there were a lot of speculators trying to play the market and make a quick buck in the expectation that prices would continue rising.

Instead, demand has crashed. Today, there are no buyers to meet the supply.

Recent reports indicate that Google searches for “can’t sell my house” just hit an all time high, surpassing the peak of the crash of 2008. Housing sales have dropped by 32% from 2020 to 2026 while supply has spiked. Realtors have been warning of a massive slowdown, with many sellers refusing to cut prices as they struggle to find interested buyers.

The struggle isn’t just with unaffordable prices.

The 2008 housing crisis vs. today

The reason for the impasse and the frozen market is largely because of debt. In 2008, the crash was caused by huge mortgage loans made to people who simply didn’t have the income to cover costs. Many of those “no income, no assets” (NINA) or “liar loans” were adjustable-rate mortgages that started cheap and got increasingly expensive over time. An entire generation of homeowners became speculators, betting on continually rising prices, steady demand and easy refinancing to keep them afloat.

Millions of homes were sold to people who couldn’t afford them. The moment home prices stopped rising and additional loans weren’t available, they defaulted all at once. Mortgage-backed derivatives began collapsing, then, like a row of dominos falling, mortgage lenders and banks and non-depository financial institutions worldwide imploded.

And a series of central bankers worldwide set interest rates to zero for 15 years. Mortgage rates are heavily influenced by central bank rates, and a combination of sub-3% mortgage rates and falling home prices lured millions of families back into the housing market.

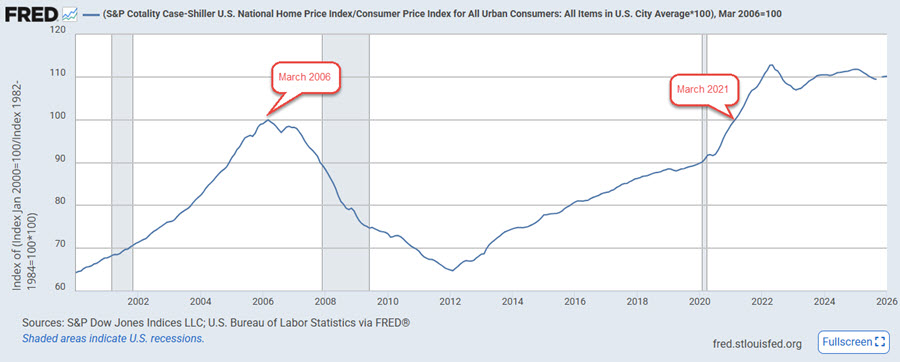

Home prices recovered – very slowly. In fact, when we adjust for inflation, nationwide home prices didn’t recover their March 2006 peak for 15 years!

There are a number of lessons we can take from this…

First, buying an asset at the peak of speculative bubble pricing is terribly destructive.

Second, even with all possible support from government programs – federal loan programs, tax deductions for home mortgage interest, grants and so on – it took 15 years for home prices to recover. That recovery was never guaranteed, either.

Third, two factors dominate prices: Supply and demand. Other forces can affect prices marginally, but supply and demand are the king and queen of prices.

Despite that eventual price recovery, today’s housing market is significantly different.

Millions of homeowners enjoy an ultra-low mortgage rate locked in during the Bernanke or Yellen years. Collectively, we’re sitting on some $17 trillion of total home equity. About $200,000 per household. But it’s inaccessible. A home equity loan (HELOC) costs at least 7% today according to BankRate, usually much more.

Families who own properties are sitting on significant value appreciation. Usually that would result in “trading up” – selling the home to buy another. But today, that’s a terrible idea – because it means trading a 3% mortgage for one more than twice as expensive (6.4% today, again via BankRate).

So they don’t sell. It’s not a winning proposition.

Worse, too many bought during the worst of the pandemic panic – when prices were highest. Take another look at the chart above. You’ll note the May 2022 price peak hasn’t yet been matched.

So many families are stuck trying to sell $250,000 homes for $600,000, and $500,000 homes for over a million dollars. The problem is, no one wants to pay $600,000 for a $250,000 home – especially when they have to finance it at 6-7%.

Excessive prices destroy demand. Now, in most markets, a mismatch like this results in falling prices.

Housing, though, is different. The majority of homeowners cannot discount their homes when they want to sell. That would be essentially the same as taking on even more debt. Whether or not they live in the home, they still owe the bank.

As a result, the housing market is frozen. Turnover is at a 30-year low. There are 50% more sellers than buyers. It’s a mess.

Really, there are only two options left:

- Put excess homes on the rental market

- Cut prices dramatically, sell and take the loss

I expect this trend will accelerate within the next year, even if there is government or central bank intervention.

Inflationary stimulus is not going to save the housing market this time. And I don’t see 50-year mortgages as an affordability solution.

What happens when home prices fall?

Falling home prices means considerable losses in home equity and overall net worth of the population. The average American family’s net worth is 50% home equity.

Just like in 2008, falling home prices means tighter credit – fewer mortgage loans made, and less lending overall. Reduced credit access means a retail slowdown, especially today, considering how strained most families’ financial position already is.

Here’s what concerns me: Where there is no liquidity, there is a crash in prices.

Price drops of 30%-50% are possible (and well overdue). For people waiting to buy, this could be good news.

Property owners will likely wait out the storm until they think prices have hit bottom.

In the meantime, there is a danger of systemic risks – not just to mortgage lenders and banks, either. Systemic risks that extend into every corner of the financial system. From the already-troubled private credit sector to “too big to fail” global megabanks…

Just like 2008.

Actually, it won’t be a repeat of 2008 – because the financial system is significantly more brittle today…

The Federal Reserve’s balance sheet quadrupled, from under $1 trillion to $4.4 trillion back then. Today the Fed already has over $6.6 trillion – they really can’t stimulate much more than that.

In 2008, federal government debt sat at $8.4 trillion – today? Over $39 trillion (and counting).

Household debt is 80% higher today than in 2008. Corporate debt has doubled over the same period.

The global situation is significantly more perilous than in 2008.

As noted, it’s not just the U.S. facing a housing market crash. Reports suggest conditions are even worse in Canada, Australia, the UK and most of Europe.

In the UK, housing for median income earners (also known as “the middle class”) barely exists, even if they want to rent.

In Australia, the median home price is around $700,000 (vs. $415,000 in the U.S.).

Back in October, the famous British newspaper The Economist published a special report with the title Governments Going Broke. It’s well worth a read. But I’ll save you some time and hit the highlights:

- The world has never been more indebted than it is today

- As debt increases, interest rates tend to increase as well (making debt more expensive)

- History shows us that economic growth rarely solves this problem…

- …and that big, rich countries have rarely repaid debt from budget surpluses

- Because sovereign debt is nearly always either defaulted on or inflated away, loaning indebted governments money is a losing proposition

Investors will be looking for a safe haven alternative. Property used to offer a safe haven from a debt- burdened financial system, but as you can clearly see, that is no longer true.

There are very few secure assets left in this environment. Physical precious metals is one of them.

This is brings us back to the crash of 2008, which eventually led to a historic surge in gold and silver price. In many cases when property no longer represents a secure asset – especially when the financial system is in a panic – that’s when precious metals become the must-have asset. When demand explodes, prices follow. Innovation sometimes follows, too – famed Swiss refiner Valcambi developed the CombiBar in response to massive gold and silver demand in the aftermath of the 2008 financial crisis. Investors wanted the security of 2-3 oz. of gold bullion in their pockets. Just in case.

Despite the wild fluctuations in the past couple months, gold is still up 236% since 2019 and is extremely likely to continue climbing when housing prices fall. The reason is simple: Total debt continues to grow despite central bank interventions and higher interest rates. These measures were supposedly meant to reduce consumer borrowing, but that didn’t happen.

And, as debt grows, precious metal values invariably climb. And it’s easy to understand why! Debt and credit essentially create purchasing power from nothing – out of thin air. That logically devalues purchasing power – because the supply (of money) has increased, but the supply of goods and services to spend it on has not. Because commodities like crude oil, gold and silver cannot be magically created, their price tends to rise when purchasing power falls.

There’s really no escaping this trend – unless you want to move to a third world country. (Ironically, those people are not too happy to see Westerners moving into their towns right now…)

It’s doubtful that central banks, built entirely on Keynesian interventionism, will allow housing prices to fall to equilibrium. They will step in with more stimulus eventually, which, again, implies ever increasing gold and silver prices.

For now, the smart move for people looking to buy property is to rent until this process plays out, and diversify with physical precious metals in the meantime.

The Best “Go Paid” Deal on Substack! You Get REAL Stuff!!

Go paid at the $5 a month level, and we will send you both the PDF and e-Pub versions of Etienne’s new book: To See the Cage Is to Leave It - 25 Techniques the Few Use to Control the Many and a coupon code for 10% off anything in the https://artofliberty.org/store/.

Go paid at the $50 a year level, and we will send you a free paperback edition of Etienne’s new book: To See the Cage Is to Leave It - 25 Techniques the Few Use to Control the Many OR “Government” - The Biggest Scam in History… Exposed! OR a 64GB Liberator flash drive if you live in the US. If you are international, we will give you a $10 credit towards shipping if you agree to pay the remainder.

Support us at the $250 Founding Member Level and get a signed high-resolution hardcover of “Government” - The Biggest Scam in History... Exposed! + Liberator flash drive + a signed high-resolution hardcover of Etienne’s new book: To See the Cage Is to Leave It - 25 Techniques the Few Use to Control the Many + everything else in our “Everything Bundle” of the best in voluntaryist thought delivered domestically. International pays shipping. Our only option for signed copies besides catching Etienne @ an event.

Comments ()